Use this full guide to register UAE Corporate Tax on EmaraTax. Addresses deadlines, fines, waivers, documents needed and guided registration.

This is a Step-by-step corporate tax registration UAE on how to actually register Corporate Tax with EmiraTax, who is required to register, the official deadlines, penalties (and the existing penalty-waiver program), required documents, timelines, and frequently asked questions.

What is UAE Corporate Tax?

UAE corporate tax law is a Federal Tax Authority UAE registration of business profits of juridical persons (companies) and some natural persons engaged in a business in the UAE. The normal 9% is on taxable profits exceeding the AED 375,000 mark; 0 percent below the mark. The legislation became effective in terms of financial years that began on or after 1 June 2023. Free zone persons may be qualifying free zone persons (QFZPs) who may receive a 0% rate on qualifying income under certain conditions; otherwise, non-qualifying income is taxed at 9 percent.

Note: Corporate tax is not the same as the Vat in UAE and Excise. EmaraTax registration process is a digital platform of FTA where registration and obligations are done.

Who should be registered to UAE Corporate Tax?

You must register if you are:

- Resident juridical person (LLC, PJSC, PSC, and so on) in the UAE.

- Non-resident juridical person that has a Permanent Establishment (PE) or Nexus in the UAE (e.g. deriving UAE-sourced income via a Nexus, such as immovable property).

- The natural person (individual) that has a business or business activity in the UAE with an aggregate turnover exceeding AED 1,000,000 in Gregorian calendar year (wages, personal investment income, and real estate investment income not in a licensed real-estate business are not to be included in the calculation of the turnover).

Exempt Persons (e.g. entities in government, qualifying public benefit entities) may yet be obliged to register at the request of the FTA.

Always confirm your category before applying.

UAE Corporate Tax Registration — A to Z in EmaraTax

Below is the end-to-end process exactly as it works on the FTA’s Business tax compliance in UAE EmaraTax portal. You can perform this from desktop or via the EmaraTax mobile app.

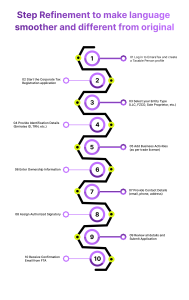

A. Before You Start: Checklist of Information & Documents

For all applicants

- UAE Pass access (recommended) or email + mobile to create / log in to EmaraTax.

- Legal name (English & Arabic if available), trade/industrial license details, date of incorporation, legal form, establishment/branch structure (if any).

- Financial period (start/end), first tax period start date, expected revenue.

- Registered address and contact details.

- Authorized signatory details (Emirates ID/passport) and proof of authorization (POA/board resolution/MoA as applicable).

Officially required uploads (per FTA service card):

- Natural person: trade license (if any), Emirates ID/Passport.

- Legal person: trade license, Emirates ID/Passport of authorized signatory, and proof of authorization for the signatory. (Accepted file types: PDF/Word; 5MB per file.)

B.Create or Access Your EmaraTax Account

- Go to tax.gov.ae → Services → Corporate Tax Registration → Start Service, or log in directly to EmaraTax.

- Sign in with UAE Pass (fastest) or create an account using email + mobile through OTP Verification

- Complete your profile, set security questions, and confirm contact details. (The FTA emphasizes EmaraTax for all CT services.

C. Create/Select the Taxable Person

- On your EmaraTax dashboard, create a “Taxable Person” profile if this is your first time:

- Choose Juridical Person (company) or Natural Person (individual running a business).

- Enter legal/registered name, trade name, and license details (number, issuing authority, first license issue date, latest renewal).

Emaratax Dashboard:

- For groups with UAE branches: remember UAE branches of a domestic juridical person are not registered separately; they follow the parent entity.

D. Start the Corporate Tax Registration Application

- In the Taxable Person view, choose “Register for Corporate Tax.”

- Business Identity & Structure

- Confirm Tax residency requirements UAE (resident/non-resident), legal form, Is Free Zone Person? and (if relevant) intention to meet QFZP conditions.

- For non-residents, disclose Permanent Establishment or Nexus details and the date created.

- Financial Information

- Set your first tax period (start & end dates) in line with your financial year (e.g., 1 Jan–31 Dec).

- Provide accounting basis (IFRS or IFRS for SMEs) and expected turnover.

- Addresses & Contacts

- Registered office address (UAE) and principal place of business (if different).

- Primary and secondary contact details.

- Authorized Signatory

- Add the authorized signatory (Emirates ID/passport).

- Upload proof of authorization (Board Resolution/POA/MoA clause) per company policy.

- Attachments

- Upload the trade license, ID/Passport, and authorization proof. (PDF/Word; ≤5MB each.)

- Review & Declaration

- Confirm all details, tick the declaration, and submit.

E. After You Submit

Processing time:

FTA states up to 20 business days upon a complete application being received; in case they demand additional information, you will be required to reply and resubmit (another 20 business days can be taken). In case you fail to resubmit within 60 calendar days of an information request, the application is rejected.

Once approved, you receive your Corporate tax consultants in UAE Registration Number (TRN) in EmaraTax and by email.

Fees: Registration is free of charge.

UAE Corporate Tax Registration Deadlines (including 2025)

The FTA set specific deadlines to register based on your license issuance month (for resident juridical persons that existed before 1 March 2024) and trigger dates for newer entities and non-residents. Highlights:

- Resident Juridical Persons (pre- 1 March 2024)

Deadline varies with the month when you had been initially licensed; these are till May 31, 2024 to June 30, 2025.Exemption: Your CT registration Corporate tax deadline UAE is 31 December 2024, in the case your first license was issued in July-August, 31 May 2024, in the case of January-February, and so on (Complete schedule in FTA Decision No. 3 of 2024.)

2) Resident Juridical Persons (incorporated on/after 1 March 2024)

Register within an amount of 3 months after incorporation/establishment or recognition.

3) Non-Resident Juridical Personality.

- With a Permanent Establishment (PE): Within 3 months of the existence of PE.

- In case of a Nexus (e.g., UAE-sourced income through immovable property): Within 3 months after the date nexus is established.

4) The Natural Persons (Individuals).

- Will have to be registered provided their business/business activities within the UAE generate a turnover of more than AED 1,000,000 during the calendar year from Jan-Dec.

- Deadline: 31 March of the following year in case of the exceeding of the threshold (e.g., exceed in 2024 → register by 31 March 2025).

If you’re unsure about your deadline, check your license’s first issue month (not renewal) and match it to the FTA Decision schedule, or use the “deadlines” notices in EmaraTax.

Penalty for Missing the Registration Deadline and How the Penalty Waiver Works

Standard Administrative Penalty

If you miss the CT registration deadline, the Administrative Penalty is AED 10,000 for failure to submit a CT registration application within the specified timeframe.

Penalty Waiver Initiative (2025)

The FTA has launched a temporary initiative to waive/credit/refund the late CT registration penalty if you:

- Submit your first CT tax return file (or annual declaration for Exempt Persons) within 7 months from the end of your first tax period (instead of the usual 9 months).

- The initiative applies only to the first tax period and covers cases where the penalty was levied but unpaid, paid (credit/refund to EmaraTax account), or not yet imposed.

FTA press communications in July 2025 reiterated the above and urged taxpayers to file within the 7-month window to benefit.

Note: This waiver does not shift your payment due date for any CT payable — tax remains due within 9 months from the end of the tax period; the 7-month rule is solely for waiving the late registration penalty.

How to Apply for Corporate Tax Registration in the UAE (Concise Steps)

- Log in to EmaraTax (preferably via UAE Pass).

- Create/Select the Taxable Person (juridical or natural person).

- Click Register for Corporate Tax.

- Complete entity details, residency, legal form, Free Zone status, PE/Nexus (if non-resident).

- Set your financial year and first tax period.

- Enter addresses, contacts, and authorized signatory; upload required documents.

- Review → Declare → Submit.

- Track your application in EmaraTax; respond to any FTA information requests within 60 days.

- Receive your CT TRN once approved. (Processing: up to 20 business days after a complete application.)

- File your first CT return by the statutory due date (and within 7 months if you need the penalty waiver).Corporate Tax Registration Services in the UAE (What a good Business tax advisory Does)If you prefer not to handle this in-house, specialized CT registration services typically include:

- Eligibility & structure review: Confirm tax residency, PE/Nexus, Free Zone status, and whether QFZP conditions are intended/likely to be met.

- Deadline mapping: Match your license first-issue month or trigger event (for newer/non-resident entities) to the FTA schedule so you don’t miss cut-offs.

- Document preparation: Compile license, ID/passport, and proof of authorization in the right formats; prepare board resolutions/POAs where needed.

- EmaraTax setup & application: Create the taxable person, complete all sections accurately, attach supporting evidence, and submit.

- Follow-ups: Monitor for FTA queries, respond within 60 days, secure TRN, and set up return Corporate tax filing in UAE reminders.

- Post-registration onboarding: Configure accounting cut-offs, chart of accounts for CT, small business relief assessments (where relevant), and QFZP compliance tracking.

- Penalty-waiver assistance (2025): When you have late registration, intending to submit the first return within 7 months will be eligible to receive waiver/credit/refund of the AED 10,000 penalty.

Mistakes that have to be avoided:

- Using the license renewal month instead of the first issue month to check your registration deadline. (FTA’s schedule keys off the first issue month.)

- Selecting the wrong entity type (natural vs juridical) or omitting branches.

- Wrong first tax period dates or ignoring the 7-month waiver filing window if late.

- Missing attachments (e.g., proof of authorization for the signatory).

- Assuming Free Zone = no registration. Free Zone Persons must register; QFZP status affects rate, not registration.